Last week, I started penning the first post of my personal finance concept series to help motivated individuals to understand the basic personal finance concepts. That post was mainly targeted at individuals that want to get their feet wet and to start learning how to manage their money responsibly. For this post, I am going to dive a bit deeper and continue to build on top of those concepts. I am going to discuss the everyday personal finance concepts that can help individuals who are in the wealth accumulation phase grow or protect their wealth.

So, what are the everyday personal finance concepts? Well, they are the daily money activities that are a part of our lives. Regardless if we are aware of these money activities or not, we will need to deal with them at some point in our lives. The earlier that we become aware of them, learn how to take advantage of them, the better off we’ll be. Let’s dive deeper and see what these concepts are.

Your Net Worth

To put it simply, your net worth is what you own minus what you owe. There are two important factors that we need to pay attention to when it comes to our net worth. First, is it positive or negative? Secondly, is it on an up trend? By that I mean are you worth more today than you were a year or two ago? If your net worth is negative or it’s not moving in the right direction, then it’s time to take action to make it right.

For the majority of us, we were most likely saddled with a mountain of debt after we graduated from post secondary school. I know I was. I graduated with about $30,000 of student loan debt, so my net worth was -$30,000 because I probably had nothing of value at that time. Once I got my first job, my priority was to pay off my high-interest debt (I was lucky that I had very little) and student loan debt. By slowly paying off my debts, I was building a positive trend and was increasing my wealth slowly.

Now, what if you have been working for a couple of years and can’t seem to get out of debt and still have a negative net worth? This can only mean one of three things. First, you are spending more money than you make on a monthly basis. Second, you’d rather spend the extra money left over from your pay than to save for your future. Third, you’re just not making enough money. By that, I mean that you’re not being paid at the market value for the skills that you possess.

So spend less than what you earn. Save a portion of your income first, before you spend it. Work on getting a raise or find a better paying job somewhere else that pays you what you are worth. When these three issues are rectified, you will start to experience an uptrend in your net worth.

Income Tax

I feel that income tax is an often neglected topic that people don’t really like to talk about along with money. I know that the tax code can be a very complicated topic. It can be quite a daunting task to file your own income tax. However, I believe that you don’t have to know all the ins and outs of the tax code. You just need to know two things: what actions will lead you to pay less income tax and what action will shelter your money from being taxed.

I strongly believe that increasing your wealth is not just about increasing your earnings, decreasing your expenses and making a reasonable return on your investments. Look at it this way, if you pay less taxes, you’ll automatically make more money without having to increase your income. You’ll have more money to spend. Your investment return will be higher because you get to keep more of the income earned from your investments.

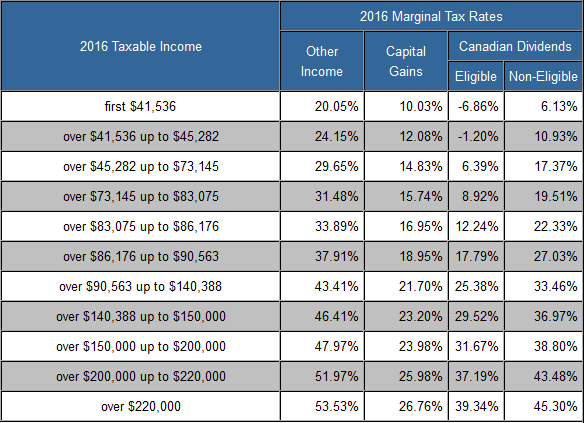

For example, I save my money in the Registered Retirement Savings Plan (RRSP). Whatever the amount that I saved (there is a limit for contributing to the RRSP account based on your previous year’s income) each year, will get tax exempted at the highest tax bracket. My money will get to grow tax-free until I withdraw. My highest tax bracket for 2016 was 43%. So when I saved $10,000 in my RRSP account, I got a tax refund of $4,300. To grow your wealth, you have to know how to use the RRSP income tax break for your own benefit.

I can spend my tax refund if I wanted to, but I chose to save that money in my Tax Free Savings Account (TFSA). For this account, you pay no income tax for any type of income that you received. Or I can give my kids a head start and invest my tax refund in the Registered Education Savings Plan (RESP). The money in this account can also grow tax-free until it’s withdrawn. Only the gain is being taxed, but it’s taxed based on your kid’s income, which is almost zero if they don’t have other sources of income.

You can boost your savings tremedously (72% to be exact) by just knowing how to use the tax benefits of the RRSP, RESP and TFSA accounts. Three things to know about taxes is not a lot is it?

Source from TaxTips – Ontario marginal tax rates.

Different Types Of Income

While I still have your attention, I want to continue on with another income tax related concept – the different types of income. There are three main categories of income: normal income, dividend income, and capital gain income. Depending on your personal situation and the source of income, you may be able to pay less income tax for each additional dollar that you earn.

Income in the form of employment, self-employment, interest and rental income get no preferential tax treatment. Every dollar that you earn gets added to what you are already earning. These form of incomes are the most tax inefficient form of income. Since Canada has a progressive tax system, the more you earn, the more tax you’ll pay. To pay less income tax, consider earning other forms of income.

Based on the income tax table from TaxTips, the most tax efficient form of income for people living in Ontario earning less than $91,831 is the Canadian eligible dividend income. This just means that the company that pays you a dividend is a Canadian based company. The Non-eligible dividends are from companies that are non-Canadian. Hence, those dividends get less tax breaks once you go over the $91,831 earning threshold. If you’re in this income range, you’ll pay the least amount of income tax for each additional dollar earned in the form of Canadian eligible dividend.

For capital gain income, it’ll be more tax efficient when your income reaches the upper tax brackets. The capital gain tax rate for the top tax bracket is 26.76% for Ontarians. Hence, if you want to earn more money and pay less taxes, the capital gain will be the category of income that you want to target if you make more than $91,831 a year.

Investment Risk VS Return

Do you know that there are risks everywhere and in everything that you do? Some activities consist of bodily harm risk, while other activities consist of financial risk. Hence, we cannot eliminate risks in our lives, but we can minimize, manage and mitigate risks. Since this blog is about personal finance, I am going to only cover financial risks.

Many people think that the stock market is very risky. They prefer to keep their money in savings accounts that pay peanut of an interest rate on their savings. Worse of all, some people chose to keep their money in the form of cash for fear of losing their principal if they invest their money and the value of their investment goes down.

I understand this fear and I know that people want to protect their savings. However, not utilizing your savings to earn a reasonable return above the rate of inflations (historical rate of inflations is about 2% to 3% on an annual basis) is also a risk. You’ll risk losing purchasing power in the future. Worst of all, you’ll risk running out of money before you die. I am not afraid of losing money. I am more afraid of running out of money before I die.

To minimize your investment risk, you’ll first have to understand the correlation between risk and return on investment. The less risk you take, the lower your potential investment return will be. However, taking more risks will not necessarily mean that you’ll make more money on your investment. It just means that you increase the potential for your investment to make a higher return. No guarantees.

So what is the appropriate amount of risk to take? The truth is, I don’t have a one size fits all answer for a specific answer for a group of people. The best course of action to take is to educate yourself, have a basic understanding of the risks and potentials of the assets that you want to invest in. At the end of the day, the riskiest investment is investing in something that you don’t understand.

Insurance

Insurance. One of the hardest topics to talk about and to understand. I was feeling pretty wishy washy when I was trying to write this section. Insurance is a different kind of beast. We all want the protection, but we never want certain events to happen to us. Hence, some people have this love-hate relationship with insurance. Okay, mostly hate and not a lot of love.

To get around the negative thought about insurance, let’s look at it from a different point of view. We buy insurance such as home, car, life, health, and travel insurance to protect us from what if scenarios. Most people don’t buy insurance as part of their estate planning because there are tons of other things to worry about in life rather than to worry about money after you’re dead.

The way that I look at it is a small investment that I am making not to become rich, but to protect myself or my family from being poor if a certain event happened. One of my main reason for buying insurance is not to protect me, but to protect the finance and well being of the people around me. As I mentioned earlier, everything we do involves risk. Buying insurance is a form of risk mitigation. Make sure that you understand the types of insurance that you need and the protection that they provide.

My Two Cents

Every day, we go to work, we earn an income, we save for the future and we pay our bills and income tax. These activities are a part of our daily lives and can greatly affect our financial health. If we take the time to understand the impact of these activities and manage them effectively, it can put us in a better position to succeed financially in the future.

So, what everyday personal finance concepts have you mastered to help you build wealth? Have I missed any other concepts that can help others in this personal finance community build or protect their wealth?

About Leo

About Leo

A lot of people I know buy insurance (life) as an investment. We have probably all heard “but it builds cash value” etc. Not a fan of using insurance as an investment vehicle. If you loan yourself the cash value, you have to pay yourself back with interest. And you don’t really have any say in the allocation of the investment. Like you said, insurance should be used for safety and comfort rather than for an investment. I think there are better ways to use your money to build your net worth.

I’m not a huge fan of life insurance as an investment vehicle either. I honestly don’t see the point. It seems as if you’re just saying into an never ending bucket. Might as well just invest the money and make it useful.

on investment & risk, the average Jane & Joe are not sophisticated that likely are not investing in securities, mutual funds, ETF’s, stocks or bonds, options to knowing or trusting a financial advisor… simply the good old reliable GIC/CD’s or high interest accounts HIA.

There are several banks in Canada with protection CDIC (FDIC in the US) with little money deposited that folks can get over 2.3% on a daily savings account (without special bonus rates or having to switch accounts every 3 months) as well as GIC/CD’s that pay over 2.5% on a 12 mth term.

It’s really straight forward for the average person to do this without worrying about market/economic turmoil, will their investment drop or will they lose their life savings.

On life insurance, been there, done that – if you need it, then term life is best

On registered plans, well makes you wonder how many folks have RRSP/401K or TFSA/IRA?

On income, well for folks that live paycheque to paycheque, are unaware of even small possibilities to save, or those who claim to sign up for bonus credit cards (maximize on those travel rewards/cash backs), to credit card arbitrage… and what about ‘manufactured spending’ or paytm…when does it stop?

It’s all so complicated for most, even some of you that read this blog

I think one of the hardest things that I’ve yet to master is the risk vs. reward. I think I continually underestimate the risks with things and definitely over estimate the rewards too often. I’m getting better but it’s definitely a concept that I’ve struggled with over the years.

Great, straight forward explanation for people to learn about personal basic finance. Thank you..

This is a really useful post to weigh out your finances and make the most. Its an excellent topic and one we should all be following to make sure our finances are in order.

Wow! What an impressive amount of information about personal finance. I did not know a lot of this information before reading your post.

Really well detailed and useful post! US tax rate is quite high to high earners in the US! I’m not a fan of life insurance and usually the payout is less than the payment in!

Wow this is impressive. I like the way you explained with all the details. Doing taxes has never a task I love but I love your detailed explanation.

I just told my daughter that the earlier I introduce her to things like investing, saving, and diversifying her portfolio, the better off she will be!! I hope she heeds my advice. I really, really do. She’s just turned 18 though, so while I can guide her on the next step towards these things, the ultimate choice has to be hers.

I could definitely use more practice in understanding these various different financial concepts. I know that their mastery is important in order to do more things in life. Thank you for a further discussion of them.

Finances so aren’t my thing. But they are very important and you explain it so well.

What an amazing guide. These are some very simple concepts but isn’t it interesting how many people don’t really comprehend these concepts in real life?

Very informational post and helpful to those that may not know a lot about these kinda things.

I like the way you explained everything . This was really informative. Thanks for sharing your knowledge

Keeping money in the form of cash is very risky. I wouldnt advice anyone to do it. If something happens to the location, the money is gone.

Very impressive take on personal financial management. It is somehow difficult to attain financial freedom especially when you do not have self-discipline and know how. This is what we all should strive to learn more about to be able to have passive income and early retirement.