After reading the title of this post, you must be wondering, “What’s going on? Did Leo’s blog get hacked or what was he smoking before he wrote this post?” No, my blog did not get hacked nor was I smoking anything (I am not a smoker). What I wanted to say is that I increased my debt by borrowing money to invest, which allows me to save more money.

How much more did I save? Over a period of nine years, I saved an extra $200,000. I will be sharing the numbers shortly.

Why Did I Increase My Debt?

About ten years ago, I had a stable full-time job and was earning a modest salary. That was the only source of income that I had and I realized that I’ll never get rich by being an employee.

Furthermore, I didn’t think that I’ll get any inheritance from my family in the future. So I asked myself, “If I wanted to achieve financial independence and not having to rely on my job for income, what can I do?” The answer was to leverage any assets that I own and try to create more opportunities to generate additional income sources.

Fortunately, I owned a primary residence and I had some equity built up in my home. That was the first time that I refinanced my mortgage by borrowing an additional $50,000 on top of my existing mortgage.

What To Do With My New Debt Proceed?

While most people incurred more debts for either personal consumption or purchasing depreciating assets such as a new car, I can only have one purpose when I incur more debts – to invest in appreciating and income generating assets.

At the time, I had two choices: either purchase a rental property or invest in the stock market. Since I started to develop a strong interest in the financial market, I chose to invest the proceed of my loan in the stock market.

It was quite a challenging and educational experience trying to build a stock portfolio similar to the one that I documented in a recent post, how I get paid by borrowing money from the bank. I almost lost all my money at the beginning due to the lack of experience with buying on margins, combine that with the 2008 global financial meltdown.

However, I remained calm, stuck with my investment strategy and weathered the global financial storm.

How Did I Save More Money?

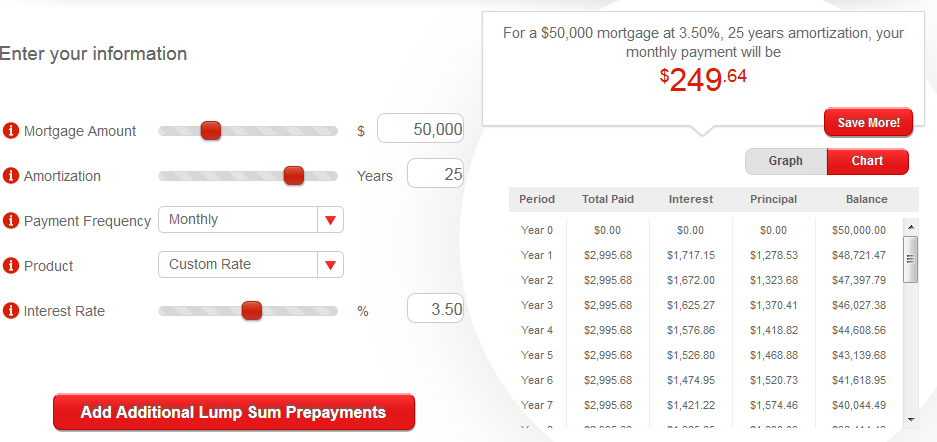

To start with, when I first refinanced my mortgage to borrow an extra $50,000 at an annual rate of 3.5% and amortized over a 25 year period, I was only paying an additional $249.64 per month on top of my existing mortgage. An amount that I felt quite comfortable with and it did not put any additional financial burden on my monthly budget.

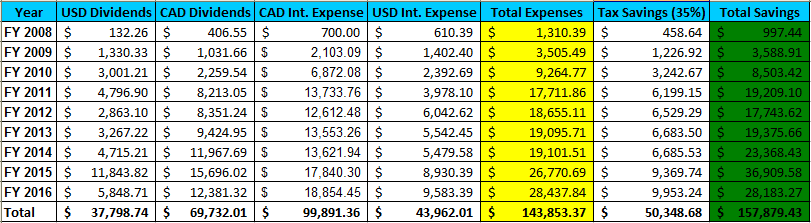

As you can see, I paid an additional $2,995.68 (= 229.64 * 12) in mortgage payments the first year, but only $1,717.15 was interest expense and $1,278.53 forced savings. How did I save the other $1,717.15? Read on…

What Are The Benefits When I Borrow To Invest?

The first obvious benefit was an additional $50,000 in stock assets that generate a passive source of income for me in terms of dividend payments. The second benefit was the principal payment went straight to paying down my mortgage rather than the $50,000 loan. Third, 100% of the interest portion ($1,717.15) of the mortgage payment was tax deductible as I used it to earn income. Fourth, the dividend income generated from the $50,000 in investments was taxed at a lowered rate than normal income. Last, but not least, any future gains from the stock portfolio will be taxed at a lower rate than normal income.

What Are The Risks?

With any types of investment, there’s definitely a certain level of risk associated with it. For this maneuver, the greatest risks are economic, market and unemployment risk. If the economy is bad and companies started to cut back their workforce, then I am at risk of losing my job. This will lead to a heavier burden of paying down a larger mortgage.

So, as long as I am employed and I don’t invest heavily in risky penny stocks, this maneuver is relatively safe. I have been fortunate to be employed ever since I started to borrow to invest.

What Direction Am I Heading?

As time goes by, I got more comfortable with investing and my employment salary continued to increase so I continued to borrow more. I started to take out personal loans from family members that are willing to lend me their money to invest. I’d pay them interest rates that are competitive with the going mortgage rate offered by the big banks.

With the real estate market rocketing over the last 10 years, I took the opportunity to borrow even more money to invest by refinancing my mortgage two more times.

What Am I investing In Now?

Based on my 2017’s first quarter financial update, I borrowed a total of $713,152.06 to invest. I categorized this amount of debt as the good debts in my book. I used some of the proceeds to build my dividend stock portfolio that’s currently worth about $529,829.98. The rest of the proceed, I used to purchase a rental property with a friend and as a down payment for a condo unit to be built in a couple of years.

How Much Did I Saved?

Earlier, I mentioned that part of my savings was paying down the principal of my mortgage. The other part of my savings came from the income tax refunds of about 35% of the Canadian dollar interests and U.S. dollar interest expenses.

On top of that, I am also getting dividend payments from my Canadian and U.S. Stocks. The combined value of the tax refund and dividends payments amounted to about $157,879.43 over a nine-year period.

I also pay down approximately $50,000 in mortgage principal during this period. Since I paid the mortgage and interest expense with my own income, I ended up increasing my savings by $200,000 over a nine-year period.

If you like this post, do it to Pinterest or follow me on Pinterest

My Two Cents

Debt can be a double-edged sword. It can help us save money and accumulate income generating assets or it can destroy our finance. If we understand the drawbacks and threats of debt, then we can use it as a tool to manage and grow our wealth responsibly. We can also take advantage of the opportunities to leverage our existing assets to further increase our wealth.

So, does your debt help you save more money or does it cost you a fortune? What’s your two cents on this?

About Leo

About Leo

Great gains Leo. We are currently residing our house and once that’s done I think we are going to refinance to invest more. I didn’t know I could write off 100% of the intrest portion if I invest it. So if we use the money to max our tfsas and rrsps can I claim 100% of that intrest for the whole term of my mortgage? Thanks and have a great easter weekend.

@PassiveCanadianIncome, when I mentioned that the interest costs are 100% tax deductible if you borrow to invest, the rule is, you can’t put it into registered accounts. So if you put the money into the RRSP, RESP or TFSA, the interests will not be tax deductible. My loans are used to either fund my non-registered brokerage investment account or used as down payment for income properties. Those are tax deductible. If I earn income in those vehicles, I also need to pay tax for the year that I earned it. Hopefully, this will clarify any misunderstandings.

Yeah definitely did. Thought it was a loophole I didn’t know about. Thanks

@PassiveCanadianIncome, if we can write off the interest on the loan and direct our money to tax sheltered investments, all the people who have money will be doing it. I am glad that we cleared this misunderstanding.

Thanks for sharing your experience. I’m always interested in reading about how people have used leverage and how it has worked out for them. I haven’t used any leverage for anything at this point, but it is always an intriguing option.

@Matt, I’ve been using leverage to help me build both my stock and real estate portfolio for about 10 years now. One advice that I would give to people who wants to follow in my foot step is to leave yourself some room for error. Don’t max out all of your loans. Make sure that you have some financial backup in case of any financial challenges that comes your way.

I do a bit with leverage but it’s primary driven when I go buy something rather then going to look for leverage. Ie I have a car loan because I can use leverage to make more then the interest rate of the loan, otherwise I would have paid cash. ISame with the mortgage, I pay extra on my mortgage to an extent but only after maxing tax free accounts. So effectively I’m still using leverage.

@FullTimeFinance, depending on your situation and risk tolerance, leveraging to earn income is not for everyone. Some people are more comfortable to leverage as much as they can (like me), while others just babble a little bit to take advantage of whatever they are comfortable with. The important thing is to know your limit and workaround it.

Wow, $200,000? That is impressive. I need to try some of this. That would be a nice amount to have, just in case.

@Amber, I honestly have not calculated the amount of money that I saved until I composed this blog post. I was kinda surprised too after I tally the number.

Once you’ve got the hang of using debt to build your asset, it’ll get easier. However, take your time to learn the ins and outs of investment and only invest in what you know.

Wow! You must have lots of guts and wisdom combined. And you’re doing good by sharing. 🙂

@Joan, in reality, it doesn’t take a lot of wisdom nor guts to do what I do. It takes discipline as you have to dedicate a portion of your income to pay the interest on the loans so that your investment has time to grow and generate the passive income for you.

If I were to remortgage my home, I think I would use the money to invest in a rental property rather than invest in stocks, like you. I am just not such a risk taker. I rather play it safe.

@Emily, everyone has a certain risk tolerance and a comfort level for different types of investments. I am glad that you’re aware of your risk tolerance and know that real estate is a better fit for you. My advice is to only invest in the vehicle that you understand and are comfortable with the risk associated with that investment.

I’m glad this worked so well for you – and that you weren’t faced with losing what you’d invested! Borrowing to invest sounds like a risky move for sure – I’m not sure I could ever be comfortable with that strategy.

@Brandi, borrowing to invest is not for everyone. For me, I felt that I have been very responsible when it comes to managing my debt. Even though my debt cost me money, it also generated income and provide tax benefits. From the summary table, the interest and savings were almost at the same level as the dividend and tax refunds. Hence, the interest that I paid were actually savings instead of expenses.

It requires guts and a lot of research to invest while in debt. Yes, the risk is high but I believe if one does his homework The investment sometimes can be the answer to living debt free!

@Muna, when you are using debt to invest, there is definitely a bit more pressure to conduct your research more diligently. Once you have done this for a while, the process becomes second nature like any other new tasks that you’ve learned.

I believe if you are a sophisticated investor like yourself debt is a wonderful tool to increase your net worth and make money. If you are the average investor I think debt can get you in a lot of trouble. Personally for me I don’t like using debt if I don’t have to but if the right deal falls in my lap in the future. It’s definitely something I’m willing to take on 🙂

@MSM, the key to using debt to invest is not to be too greedy and only borrow what you can handle. When I borrow, I know that I can always pay for the loan if I stay employed. The worst case scenario is the economy going into a recession, I lose my job and my investments are losing money. Even if that’s the case, I still think that I would be able to keep up with my debt payment for at least a year. Hopefully, I can find something within a year when the worst case scenario occurs.

Good pointers, Leo! Not sure I could ever do it myself (I’m not confident enough to fiddle around with my finances), but I’m so amazed you were able to save $200,000.

@Chloe, before using debt to invest, you’ll have to be able to get rid of all the debts that don’t help you build your net worth. Once you have control of your debt, you are now the master. Your debt will be working for you rather than the other way around. It takes some time to control your debt. Go at a pace that you’re comfortable with and ramp up the process once you get more experience.

You have different direction when it comes to investment. Not everyone can bear the risk. Keep it up your dream.

@Betty, my direction comes from my motivation to leverage my existing assets to build net worth. I also have big dreams, so it helps me to push harder to find more ways to make my dream come true.

Risky but worth to try because it’s all for saving! Will take this into consideration once I managed to get a stable job 🙂

@Aquilili, as I mentioned in my other responses, one of the requirements to borrowing to invest is to have a stable job and you’re on the right track. As for risk, it’s always manageable. Just invest in yourself first, then the rest will follow.

I love the title, it hooks the reader. Your advice is always practical.

@Stacey, I’ve been doing a little research on how to write catchy blog post titles. Thanks for dropping by Stacey.

Thanks for sharing. Nice info and good tips!

@Fatin, thanks for dropping by. Hopefully, you can make good use of the concepts presented :).

Wow, $ 200.00, definitely interesting! I should try something similar, seriously!

@Agentserozerosetter, yep. I started saving $200, then another $200 more and then another $200 more. Eventually, I reached $200,000 in nine years.

This makes sense and it is great that it worked for you! Personally I am in too much debt already to even qualify for…anything..:(

@Elizabeth, For now, just concentrate on getting rid of your debt, build up your credit history and keep this concept at the back of your mind. Once you are in a better financial situation, you can start to build your wealth. I started with $30,000 in debt once upon a time. If I can do it, you can do it too :).

Thanks for sharing such an inspirational article! Keep it up!

@Krizzia, hopefully, this post will inspire you to do more with your debt and increase your wealth along the way.

this is awesome keep posting more! good work I actually think you are very good in writing your thoughts and I learned a lot from you 😀

@Jenny, thank you for the compliment and encouragement. I will definitely be motivated to share more of my thoughts in the future.

These are some amazing tips! I’m incredibly surprised by the amount of savings you’ve made in 9 years. It’s so hard to get this started because it feels so risky.

@Sondra, to make this less risky, you’ll have to do three things. First is to have a stable income. Second, you’ll have to get rid of all the debts that don’t help you make money. Third, you’ll need to know what investments are suitable for your risk tolerance and investment knowledge.

It’s amazing that you thought to do all this. I guess a lot of people might not be willing to take risks like this but I guess it can pay off.

@Wanderlust, These are calculated risks. Even though my loans costs me thousands of interests a year, they also provided thousands in dividend and rental income. On top of that, a portion of the interests, I get it back in the form of a tax refund. Overall, it’s a zero sum game and I get sort of get a free shot at increasing my wealth depending on my investment picks.

Incurring debt to be able to make money is certainly a risky proposition if you do not know what you are doing. It looks like you had a good strategy to begin with. And that’s great that it’s working for you.

@David, before anyone following in my footstep, they need to first have a good handle on their debt. When people incur debt to the invest, they just need to ensure that they have a safety net and don’t bit more than they can chew.

Wow, this doesn’t sound like a bad idea and I believe I know a few people who have done this. I myself need to do a little more research before entering this kind of venture. Thank you for sharing your knowledge and expertise!

@Maria, doing your research before you venture into any investment journey is always the prudent thing to do. Feel free to pop a question or two in the comment section is you have further questions.

This is such a smart way to save some money!

@Payastyle, I am glad that the smart people who did it shared this concept with me. Now I am sharing it with you. Hopefully, you can make good use of it and share it with others too :).

Not everyone would think of it since loans are usually used for things that you should pay off instead of invest in. It’s a good move though and it’s a great way to increase your profit.

@Elizabeth, having the right mindset to use your debt to purchase asset rather than for spending is a prerequisite. Too often, many people got seduced by the material possessions that they can purchase once they have access to debt. In the long run, those material possessions don’t generate income and their value depreciates. This is why some people get into the vicious debt cycle.

Wow! Interesting sharing & learnt much more on how to save with loan 🙂 thanks for sharing this informative piece. Cheers, SiennyLovesDrawing

@SiennyLovesDrawing, most people associate loan as an expense, but when you used properly, it can be an asset. A lot of wealthy people have millions in debt because they use their debt to buy assets that increase in value. Everyone can do it.

Thanks for sharing Leo 🙂 I love posts like these – showing your analysis and being transparent is great.

I’m looking to buy another property today actually. I just put an offer in and we will see what happens… The RE market around my house is a little bit nuts (I heard of a house getting 18 offers the first day), but I want to get my hands dirty in some RE. This will be my second property.

As a result, I’ll have about 400k in mortgage debt but 260k of that will be rental property. Worse case scenario is I lose my job, best case scenario, I get renters in, fix up the new place, and then am able to build wealth even faster than before!

@Erik, it’s seems like you are getting more and more comfortable with your debt and are using it to build wealth. When you purchase a rental property, if the rental income is sufficient to cover your expenses, your employment status is not a big factor. However, being employed is always a good thing.

Wow i really enjoy your site. Everything is nicely organized and clean. Good content and media!

@Daniella, thank you for the compliment. Thank you for dropping by.

Thank you for this thoughtful post. It has a lot of great tips in it.

@Colleen, I tried my best to be as thoughtful as I can :).

I will have to send this article to my husband! I’m sure he will find it very useful!

@Milica, so you don’t find this article useful? Just joking. I hope that this article is useful to him.

I have an investment for my child. I think it is really important but I don’t like high risk.

@Angela, I think that risk is a personal thing. Some people thinks that stocks are very risky. It’s only risky if you don’t know what you’re doing. Depending on what you do, over the long-term, market index funds are not very risky at all.

Another knowledgeable post for me to read and learn!! Definitely there’s more for me to learn, need to force myself to start saving too!

@Sharon, It may seem like a very difficult task when you start saving. After you automated the withdrawal and never have access to your saving amount, you’ll get used to it and won’t notice the difference. The sooner you start, the more time your money has to grow.

Thanks for sharing your idea. I do agree that mostly people would get more debt to pay off another existing debt. It’s like the student loan Malaysia has. After graduating, they need to pay off the student loan and most took to personal loan or using part of their retirement money, which I think is a bad choice. It would be better to follow your idea though the stock market will be a risky choice. But hey, some risky choice gets higher return. As long as people lean of what works and what to avoid.

@Rika, it’s definitely a challenge to build your wealth if you are constantly in debt and your debt is actually costing you money rather than working hard to generate income for you. In order to use debt responsibly, one needs to earn more than one spends and get out of consumer debt. After that, one can start looking at investment debt.

“That’s a bold strategy cotton, let’s see if it pays off for him.” Little dodge ball quote for you haha. Debt is always an interesting topic for discussion. It is mostly categorized as negative hence people want to free them selves of it. But if leveraged properly it can be useful as well. You understand that the best way to create wealth faster is to do two things. 1. wealth must be in an investment account to capitalize on the lesser tax rate and compounding. 2. Leverage your time. So by leveraging your debt in order to invest young, you can accumulate more wealth by also leveraging your time in the market in the process. Nice seeing you start when everything was in a downturn. Proved a nice boost to get you started buying everything so low. Thanks for sharing!

@Dividend Daze, I couldn’t have summarized the benefit of leveraging your assets any better than what you have said. In order to take advantage of the downturn, I had to some of my emotion and fear in check. Otherwise, I wouldn’t have the courage to buy stocks when they go on sale.

THis is an interesting read. I will put this in mind.

Cheers to the share Leo. Good tips and it was a very interesting read on my part. Thank you for being clear and honest about facts like this.

I am sure not many people would have thought of it that way.. whatever it is.. great thinking!!! I wish I had your mindset

What an interesting take on this. I am going to digest this and process through it. Thank you for sharing.

@Jim, thanks for dropping by. Feel free to ask any questions. Don’t be shy.