Wow, a quarter of the year had flown by and it just seemed like yesterday that I wrote my first public net worth performance review. As I mentioned in my 2016 year end net worth performance review, every quarter end is an exciting time for me (yeah, I know. I am such a number geek.) as I love to tally the numbers and review my net worth. Now that I am on the journey to save my second million dollars, it seems a bit more adventurous and fun comparing to my first journey, which was quite boring. Similar to my first net worth performance review, I will reflect on the following areas: savings, real estate, debts, investments and net worth performances. I will share my successes and failures with you so that I hold myself accountable for my decisions and we can all learn from my shared experience.

Savings Performance

In order to grow your money, I believe that you have to develop the discipline to save money first. To develop my saving discipline I need to ensure that all of my annual financial goals are achieved on a yearly basis. My annual financial goals for 2017 are to maximize my family’s Registered Retirement Saving Plan’s (RRSP) contribution room, maximize our Tax Free Savings Account’s (TFSA) contribution room and maximize the Registered Education Saving Plan (RESP) grants for both of my kids. On top of that, I want to start to accumulate more family experiences with my family by adding a vacation fund on top of the other three saving goals.

| Items | Target | Amount Saved | Progress |

|---|---|---|---|

| RESP | $5,000.00 | $5,000.00 | 100% |

| RRSP | $17,000.00 | $2,550.00 | 15% |

| TFSA | $11,000.00 | $11,000.00 | 100% |

| Vacation Fund | $10,000.00 | $0.00 | 0% |

My 2017 family saving goals

Based on the table above, I can proudly say that we are on track to achieve our all of our financial goals this year. By maximizing the contribution to our TFSA and RESP accounts in January, that money can start to grow early. On top of that, we received $1,000 of free money (the maximum of 20% of our RRSP contribution) in education savings grant from the government. We also have an automatic 6% contribution to our work’s Employee Share Ownership Plan (ESOP) for every pay cheque. This automatic contribution is working twice as hard for us as we get a 3% matching from our employers and it’s also counting toward our annual RRSP contribution limit. By maximizing our RRSP contribution limits, we are not only saving money, we are also getting a great tax refund at the top of our tax brackets.

To ensure that more of our money are working hard for us, we directed all of our bonuses for 2016 to our RRSP accounts. Those decisions benefited us in several ways. The government has never gotten to tax that money as bonus tax sucks. We had access to invest those bonus money right away. Our savings got a huge boost without much effort from us. We get more tax refunds as we also directed that money to our RRSP accounts. As a result, I believe that this category deserves a meet expectation.

Real Estate Performance

If you’ve read a recent post that I made to emphasize the importance of doing your research when you invest in real estate, you’ll know that the real estate market in the Greater Toronto Area (GTA) is burning hot. In addition, I was trying to increase my real estate holding with a purchase of a unit in a hot pre-construction condo project. The plan did not end well as I was not able to purchase the unit that I want at a fair price. Hence, I chose to walk away instead of being ripped off by the developer.

For the past two months, I was spending quite a few weekends at my rental house and also took a few days off work to update the property to meet the city’s fire code. This period was quite challenging as I needed to juggle my full-time work, family life, volunteering at the Autism In Mind Children’s Charity, renovating my property, real estate business and blogging. My stress level was going through the roof, but I was really happy and relieved that my hard work paid off as my property passed the inspection. Even though there were not many changes in my real estate portfolio, the improvement that I made to my rental property and the prudent approach that I took to not overpaid for properties deserves an exceed expectation rating.

Debts Performance

There hasn’t been a lot of activities on this front. I had been paying all my credit card bills in full every month, paying my mortgages on time and did not incur any additional debts. One good thing that resulted from these boring activities was that I was slowly building more equities in my properties. So I’ll give this boring category a borderline meet expectation as I don’t think I’ll be doing much in this category for the near future. Maybe another round of refinancing to borrow more money to invest.

Investments Performance

The investment category had always been the most exciting for me as I spent a lot of time to try to improve my performance, lower risks, earn free money and pay less taxes. Recently, I’ve added a new item to my to-do list – generate more passive income. One of the obvious methods is to buy companies that have a great history of increasing their dividends. The other is to continue to write/sell more naked put options (stop your wandering mind, it’s not that kind of naked) on stocks that I want to buy or covered call options on stocks that I already own. If you are interested to learn more about options, check out my options basics post.

I manage about 15 investment accounts, which includes family and friends’ accounts. Whenever there is a stock that I want to purchase, I tend to spread the purchase to different accounts where I see fit. For my own accounts, I am actually taking a lot more risks than other accounts and I am continually refining my strategies. For other accounts, I tend to take a more conservative and cautious approach as I need to be more prudence with other people’s money. I am a little jealous that some of the accounts have a better rate of return than mine.

| Option – Contracts | Ticker | Expiry Date | Strike Price | Premium | Status | Return |

|---|---|---|---|---|---|---|

| Covered Call – 1 | CMG | January 19,2018 | $600.00 | $1629.00 | Active | +39.33% |

| Covered Call – 4 | MCD | January 20,2017 | $135.00 | $1,484.00 | Expired | +100% |

| Naked Put – 2 | EXR | March 17,2017 | $80.00 | $928.00 | Executed | -30% |

| Naked Put – 2 | GS | January 20,2017 | $135.00 | $1,597.52 | Expired | +100% |

| Naked Put – 5 | KO | January 19,2018 | $38.00 | $1,150.00 | Active | +43.09% |

| Naked Put – 3 | WFC | January 20,2017 | $43.00 | $646.29 | Expired | +100% |

| Naked Put – 3 | WMT | January 19,2018 | $65.00 | $1,335.00 | Active | +33.41% |

Options sold during 2016.

Last year, I mentioned that I wrote seven options. Three options (GS, MCD, and WFC) expired worthless this past January, so I made a few bucks in free money. Three more options (CMG, KO, and WMT) still have about 10 months to go before they expire on January 2018. I will be more than happy to buy the stocks if the price of those stocks on the put options ever dropped below the strike price and to sell the stocks if the price of the stocks on the covered call options moved above the strike price. The last of the seven options was a naked put option for EXR which I need to purchased because the price dropped below $80 in March of this year. For this transaction, I am currently losing a few dollars per share. Overall, my options were performing well.

| Option – Contracts | Ticker | Expiry Date | Strike Price | Premium | Status | Return |

|---|---|---|---|---|---|---|

| Covered Call – 2 | CAT | January 19, 2018 | $110.00 | $628.00 | Active | +42,68% |

| Covered Call – 4 | MCD | January 19, 2018 | $140.00 | $764.00 | Active | -17.80% |

| Covered Call – 5 | WFC | January 19, 2018 | $65.00 | $965.00 | Active | +52.33% |

| Naked Put – 5 | ENB | January 19, 2018 | $50.00 | $935.00 | Active | +30.48% |

| Naked Put – 3 | MRU | September 22, 2017 | $38.00 | $361.30 | Active | +46.03% |

Options sold during the first quarter of 2017.

After the expiry of the options in January for the options that I wrote last year, I once again wrote more covered call options for some of the U.S. stocks that I own (CAT, MCD, WFC). I also wrote a few naked put options for (ENB, MRU) as I want to buy those Canadian stocks at a lower price. I am hoping that all my covered call options get executed as I want to cash in some of my gains. If not, I am still making free money from the option premiums and continue to collect dividends.

At the end of last year, I still have about $45,000 in cash that I still need to put to work. As I mentioned earlier, I will be focusing on dividend paying stocks going forward so I bought all the dividend paying stocks listed in the above table. For some of the accounts, I also shifted my focus to index ETFs. Most of the extra cash were deployed, and now, I just sit back and collect the dividends and watch my money grow.

This quarter, I was mostly cleaning up my accounts by shifting low paying dividend stocks from my TFSA and RRSP accounts to my taxable account. I was selling the same stock in my TFSA and RSRP accounts and buying them back in my taxable account. At the same time, I am also adding more higher paying dividend stocks to my TFSA and RRSP accounts so that those dividends can be tax sheltered. So these boring activities in this category get a boring meet expectation rating.

Net Worth Performance

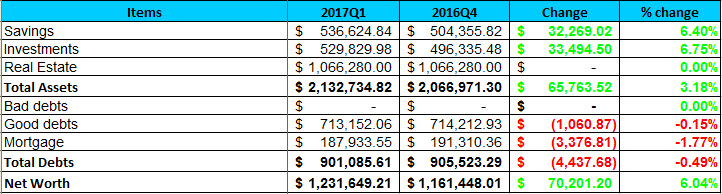

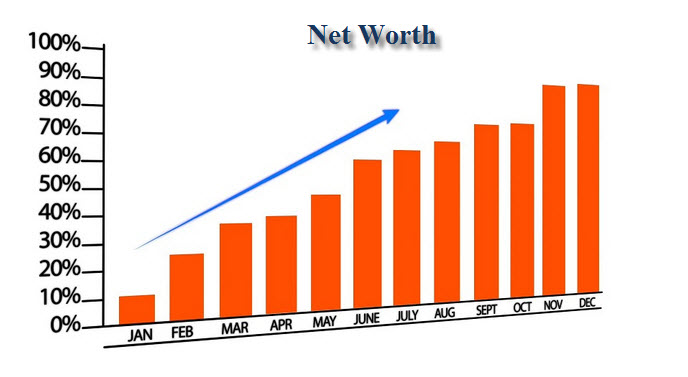

From a quarter to quarter point of view, I don’t pay much attention to the movement of my net worth. I prefer to assess my net worth performance on an annual basis. I think that it’s a better measure. Based on the table above, performance of my net worth is performing well (+6.04%) comparing to the return of the S&P TSX (+1.70%) and S&P 500 (+5.53%) index. My 2017 net worth goal is to reach $1.3M by the end of the year. At this pace, it seems achievable and hopefully, my performance can continue to improve. Hence, I’ll give this category a meet expectation.

2017 Q1 Overall Performance

Overall, I have been performing relatively well in the savings and real estate categories. I hope that I can continue to maximize my TFSA and RRESP contribution at the beginning of every year. I also hope to complete the transformation of my current investment portfolios into a high dividend yield portfolio consisting mostly of stocks that have a strong dividend payment history. Since my goal is to increase my net worth by 10% annually, I only need to increase my net worth by approximately 2.5% per quarter. Hence, a return of +6.04% is definitely exceeding my set expectation.

So, how often to you conduct your net worth calculation? What financial goals do you set for yourself? How do you balance your current lifestyle with saving for the future?

About Leo

About Leo

Hey Leo. Nice update. Fantastic work maxing your tfsa and resp’s right off the bat. Those options are doing great. Here’s hoping enbridge go’s to 50$ soon. I do our net worth every month. It’s great to see the progress and keeps us motivated.

@PassiveCanadianIncome, my options are doing well. If my cover call options get executed, I’ll be make at least 15% for those trades on top of what I have already gained. Anytime that I can write covered call options that can provide me with at least 15% within a year, I’ll write it. I also get the premium up front. It’s a great way to beef up your passive income on top of dividends.

Very interesting and informative. I will see if I can apply the things I learned here where I am located.

@Ralin, net worth tracking can be done by anyone living anywhere. Just be honest with yourself when you are estimating the value of your assets. 🙂

good info. learn something here!!

@Geozo, thanks for following my second million dollar journey. Hopefully, it can inspire you to start your own journey to save whatever amount that allows your to be financially freed.

Thank you for sharing your quarterly report. I can see good progress there. I am not as meticulous as you and do not have a report. I just know that I have + sign every month end.

@Emily, having gains from month to month is definitely good. Let’s just hope that our gains in assets are faster than our gains in debt.

interesting to read about this. I learn something new today.

@Sherry, I am glad that you have something to takeaway from this post. I strongly feel that these reports are more about the decisions that I made to improve my net worth rather than the change in the numbers.

Congrats! Looks like a great quarter for you. Nice work maxing out the RESP and TFSA already!

@Matt, I was lucky to have some leftover cash from the end of last year and was able to distribute to the account that will reap the benefit of early starts. Getting free money from the RESP contribution is also a bit of a motivation for me too.

Congrats! It’s a good thing that you’re contributing to RESP for your kids 🙂 My parents did for my sister and I and it definitely set us off on a good financial start after university. I do a net worth calculation on a monthly basis… as a self assurance that it’s not going down! Right now on the balance of “current lifestyle” vs “saving for the future”, we’re still tilting more towards current lifestyle, with the caveat of at least putting money into tax advantaged accounts. Hoping to go more the other way as we get older and settle down.

@Song, when I graduated from University, I was in about $30,000 of student loan debt and it took me quite a while to dig myself out. The beauty of the RESP account is the free money and tax deferred growth. I am hoping that the RESP account will have made enough gains that my kids can use the capital gain from the account for the tuition and I get my principal back when they start University.

Wow this has been a great quarter for you. Anytime investments are going up and debt is going down are times to celebrate 🙂 Looks like you are well on your way to the 2nd million.

@MSM, having the first million as a base really helped kick start my second million quickly. It took me about 5 years to get from $0 to $200,000, but only about one year from $1M to $1.2M. Having a much higher salary comparing to 10 years ago also helped too. So how did you do? Hopefully the recent increase in Chipotle Mexican Grill’s stock price helped you a bit.

Wow l Love the great insight of your Net worth performance. I have Learned a few things from your post. I have read about people who could pay off their student Loan and still live a successful Life, and you are one of them.Thanks for sharing

@Klea, I can honestly say that by conducting a net worth performance review, it helps me reflect on my decisions for the past three months. If I did not perform very well in any of the areas, I make sure that I pay more attention in those areas and try to improve in the the future.

you are definitely an inspiration… i do not know if I can be like you but these are definitely a few things to ponder on…

@Miera, it takes a little of time to figure out exactly which part of the net worth equation that you are most comfortable working on. Some people just can’t stand debt and they’ll do everything to try to pay it off as quickly as possible. For me, I like to investigate any variable that can help me boost my net worth.

Wow, such a good info here.

@Emilinda, thanks for dropping by. Hopefully, there is something in this post that can help you improve your net worth.

Wow thanks for sharing these tips and trade, will pick up more from here.

@Kelly, thanks for dropping by. I hope that these tips will serve you well.

nice sharing. i should learn from you as goals is important. 🙂

@Qian, goals are definitely important. It keeps me on track and it motivates me to push harder to achieve more. Thanks for dropping by.

This is very helpful to determine how much i am valued 🙂

@Blair, glad that it’s useful to you. Thanks for dropping by.

Impressive and inspiring. I love how you break out bad debts and good debts! 70k in a quarter is a great increase in wealth.

I grew my wealth about $16k in Q1 2017 – it should only increase from there each quarter!

Thanks for sharing Leo.

@Erik, being able to identify good debt is important as I consider good debt an asset. All of my good debts are either helping me earn more dividends or generating rental income.

A very informative sharing here, learnt lots of knowledge & enjoying reading it 🙂 cheers, SiennyLovesDrawing

@SiennyLovesDrawing, Glad that you enjoyed reading it. I try to share the tricks that I use to earn more money with others in these posts rather than just give readers a table of numbers to look at.

Wow. You have a really solid plan for growing your wealth. My husband and I would love to add real estate investing to our financial plan, but I’m a big chicken!

@Heidi, real estate is not so intimidating as long as you have the knowledge. Here are a few post from my blog to help you boost your real estate knowledge.

My husband is an accountant, so he is on top of all this stuff. I think he recalculates our net worth every quarter.

@Robin, I am not sure that if this is a men thing, but I find that in my circle of friends, the men tends to do all the financial management in the family. At the end of the day, it doesn’t matter if it’s the wife or the husband, as long as there is one spouse managing the family finance responsibly is sufficient. Two will be ideal.

You are doing awesome! I’m slowly working on growing my wealth. Slowly. But surely, ha.

@Amber, slow and steady wins the race. There is nothing wrong with that. Just keep on doing what you are doing as long as you are comfortable with the pace.

Definitely need to learn all this from you! I don’t always plan and do this!

@Sharon, you don’t have to do a full blown net worth calculation every quarter. Start with baby steps by concentrating on one or two things at a time and slowly add more on top. People usually start with either debt or savings.

I definitely think that saving money is one of the most difficult thing for people to do specially nowadays because so many people are living paycheck to paycheck. This is super inspiring thank you so much for sharing!

@Sandra, Saving money can be difficult if you don’t have any motivations or goals. For me, my goal is to retire by the age of 48. My motivation is getting free money from the government when I save. Find your motivations and goals. It’ll be easier as time goes by.

This is so fascinating to me since I’m just beginning to learn about investing and personal finance. I wish they taught this stuff in schools because now I’m in my twenties and just beginning to figure this stuff out!

@Nellwyn, funny that you mentioned it. I also feel that the governments are not providing enough financial literacy curriculum in our school system. Here is a post that I just wrote on financial literacy.

Great job! It looks like this has been a successful quarter overall for you – good luck in the next one as well!

@Brandi, this quarter has been great. With a seven-figure stock portfolio, whenever the stock market does well, I’ll ride on its coattail. I hope that you had a great quarter too.

You have done such a great job with your savings and investments. You are quite an inspiration and thank you for sharing your report with us.

@Jessica, thank you for the kind words. One of the reasons that I share my finance is to inspire others to take control of their money. With a little time and effort, anyone can do it.

This is truly impressive. It’s good to see your savings put to good use and with the rate that you’re going, I’m pretty sure you’re going to achieve your goals in no time. Best of luck and thanks for the tips, I picked up a lot by reading this post.

@Amanda, I hope that you can also use the same tips and tricks to improve your finance too. As long as the stock market doesn’t pull another 2008 financial crisis, I have confidence that I can achieve my goal of reaching $2M by the age of 48.

That sounds great. It’s nice to see people putting their money to good use to improve their lives. I would love for my kids to read this post, or even your whole blog so that they can learn a lot more about how to grow their savings. They’re both working now.

@Elizabeth, thank you for sharing my post with your kids. I hope that my blog will resonate with them and inspire them to follow in my footstep to manage their money responsibly.

Awesome! It really takes discipline and determination to save your money and keep investing. I love being able to save especially since it allows me to be able to travel and see more of the world.

@Carol, we all have our reasons and motivation to save and invest. Traveling and seeing the world is definitely a great motivator. I would love to do that one I have achieved financial independence.

This is inspiring! I think that all of us spend so much money every day and at the end of the day don’t realise where all the money went. My wife and I spend a lot on traveling. Just a few days ago we made a plan to save money and hope to manage that. I found some useful tips in your blog.

http://www.tripblogpost.com

@Igor, The key to growing your wealth is to know where you spent your money. Start to pay attention to spending that doesn’t bring a lot of value to your life and try to minimize those spendings. You’ll be surprised that it’ll create more cash flow for other items.

Wow so inspiring to read! I do believe that saving and spending money on the right things is imperative.

@Kim, you are definitely right on spending money on the right things. I am quite willing to spend the money if it’s adding value to my life.

Congratulations, you sure are well organized and determinated! This is so inspiring, it’s always good to save money to reach greater goals!

@Agentszerozerosetter, Retiring early is definitely a big goal of mine. Once I crunch the numbers and realized that I can do that by the age of 48. It’s more motivating than ever.

Congratulations. Looks like you are on a roll. Saving this post to learn more for myself.

@Aish, Hopefully, this post will serve you well in the future.

Congrats on getting on track with your financial goals! The real estate market here is also pretty insane, especially with there being a shortage in inventory for a popular price point. Trying to scoop one up to fix and resale at a profit later has proven to be difficult!

@Cameron, in a seller’s market combined with a shortage of supply, it’s definitely difficult to land a bargain property. In my area, houses are selling like hot cakes regardless of the condition. I feel lucky to own a home.

Investment need a lot of passion and time. Hope you achieve your 2nd goal.

@Betty, if you have the passion to, you’ll be able to find time to invest easily. My second $1M is progressing well, but I know the ride will not be smooth forever. I am ready for the bumps along the way.

It is great that you have managed to incur some massive savings so far. For me I have always found my finances a struggle to master x

@Ana, the key to building your savings is to do it automatically with every pay cheque. After you get the hang of it, just start learning how to invest, or ask a friend who knows how to invest and ride his/her coattail.

Wow! This is quite informative, yet great plan to see in terms of wealth in life. That’s great to see that you’re able to manage properly and wisely. Now, I’m starting to think about my net worth. Great accomplishment for you!

@G&D, I am happy to hear that my financial performance post had inspired you to think about your own net worth. Hopefully, you’ll also be inspired to join the journey to save a million dollars too.

Hi leo, great to find your blog, it’s an interesting one for sure & congrats on your progress. What is your pie in the sky target, is it $5 mil or $10mil, or would you be OK with $2.5 mil?

Could you please explain why your good debt is higher amount than the investments?

What are the savings comprised of & if there is cash there that can pay off the mortgage, would you consider doing that, then leverage HELOC against the house?

Or are the investments cash & other and that the good debt is also used leverage the investments?

Thanks

@John, these are great questions. I will try to answer them as best as I can.

First of all, I don’t have any high in the sky numbers as I am trying to reach the $2M mark so I can retire early. Currently, my projected retirement age is 48. If my net worth is ever going to go over $2M, it’s just icing on the cake.

Secondly, the reason that good debt is higher than investment (this is the total value of my non-registered brokerage account) is because I used some of the proceed to invest in rental properties. One is currently tenanted, and the other has yet to be built.

Third, the total value of my savings comprised of all my family’s registered accounts: RRSP, RESP and TFSA accounts. I only keep a minimum amount of cash in my chequing account. Since I am borrowing to invest, if I have cash lying around, then it means that it’s not working hard to help me earn more money.

Lastly, I am leveraging my assets to invest. I refinanced my principal residence’s mortgage to borrow more money to invest in stocks and real estate. This is a better method for me as I only pay an annual interest rate of 2.59% for the loan and the interest rate is constant for at least 5 years. On the other hand, for a HELOC, the interest rate is 3.2% and it goes up if the prime rate goes up. Hence, I don’t think I’ll ever want to pay off my mortgage.

One more thing, my non-registered investment account is a margin account. I use the margin to buy U.S. stocks to hedge the currency risk. You can say that this is using my asset to leverage additional investments.

@ Leo, thanks for replying on what is what on the assets and debt.

Great blog and lots of helpful insight information Leo, thanks.

I have a few more questions which I trust you won’t mind answering, and for this discussion is it OK if I label the non-registered stock/options part of the “investments” to call it the ‘stocks’, this way separating it out from any real estate investments?

I trust my understanding in the following makes sense

Purely on the $530k of investments, these as you mentioned are outside the registered accounts. How much of that amount in 2017 or YTD is in stocks vs real estate – then, how much in dollars of the ‘good debt’ used towards the stocks investments?

Investments = $530k – $ ??? real estate = $ ??? stocks

Good debt = $713k – $??? real estate = $???stocks

In 2016, or the first quarter 2017, what was you average net percentage return after servicing costs of just the stock investing?

When and how do you decide to change your holding in the non-registered trading account & suppose on the the positions that drop from what you purchased them for, what is your strategy on that?

Do you have a hard fast rule on how many stocks you hold at any one time?

On CMG that you have the long covered call, on the basis that you are not called, will you continue to hold that position to then sell another covered call, or at what point would you sell the position to move to something else?

Do you have a percentage gain rule to exit a position?

Is the $1.066 Mil real estate just the family home, or does it include any of the investment real estate?

@John, I am more than happy to answer any questions that any of my reader has and I will try to share and be as transparent as I can.

In my breakdown, investments is pretty much the net asset value of my non-registered brokerage account + cash that I have yet to deployed. So the $530K doesn’t include any real estate holdings at all.

The $1.066M in real estate value is the estimate value of my principal home, which was pretty conservatively appraised by me. From what I see in terms of the recently sold home values in my area, I can say that my appraised value is about 20% to 25% under the current market value. In addition, it also include the value of two investment properties at cost. The reason that I include it at cost is because it’s hard to evaluate the value from a quarter to quarter basis or even year to year basis.

In terms for my division between real estate and stocks, it’s about a 25/75 split for the $713K that I borrowed to invest. When I view my investment portfolio, I think that everything that I own, make up my portfolio. So my principal residence, investment properties, non-registered accounts and registered accounts makes up my portfolio. I don’t view them as a separate portfolio. Overall, when everything is accounted for the real estate and stocks becomes a 50/50 split.

As for calculating the net return of my portfolio, I haven’t done it at all. There are a few reasons. First, my wife thinks that I spent too much time on my investments. Secondly, only the stock portion of my investment is easy to evaluate because there is a market price every day. However, there is none for my real estate holdings. Third, since I manage my all my assets one portfolio, it would be hard to separate the return from my non-registered accounts from my registered accounts and real estate holdings. I also do quite a few things to ensure that I maximize my net worth and tax efficiency of my investments rather than trying to maximizing the return of each account.

For my registered account, I tend to be more conservative and purchase higher dividend paying stocks and take less risk. For my registered account, I tend to experiment more and take more risks. From time to time, I’d sacrifice the performance of one account and restructure my portfolio to be more tax efficient. For example, I have a losing stock that I own in my RRSP account, I still want to own it. So I sell it in my RRSP account and buy it back in my non registered account.

This maneuver sacrifice the performance of my RRSP account in the short term and may provide a better return to my non-registered account. However, since I still own the same stock and the same quantity, it does not affect my net worth. However, in the long run, the money that I make on this losing stock, will only be taxed at capital gain (50%). On the other hand, everything in my RRSP is taxed as normal income regardless of how the money is made.

As for the rule for when to sell your stocks or what percent do I have to gain in order to exit a stock or how many stocks to own. I don’t have any specific rules, but I think I own too many stocks at the moment. I will try to concentrate on a maximum of 25 stocks and get rid of the rest. What I do is from time to time, I would evaluate the stock against its peers in the same industry and alignment with my strategy. For example, I have been gearing my strategy toward purchasing stocks that pay me a good dividend and with annual increases. So I sell my Rogers Communication stocks and buy BCE. The reason behind it is that I believe that BCE had been doing a better job at increasing their dividends on an annual basis and paying me a better dividend than Rogers.

For CMG, I do believe that they will have potential in the long run if they fixed their food quality issue. If my option is not exercised in January 2018, I will sell another covered call. For the premium that I got (about 4%), it’s just like receiving a dividend. If the stock sky rocketed after I sell my call option, I still won’t feel too bad because I will make at least 15% on it. Whenever I can make more than 15% on an annual basis on any transaction, I am content and happy to make that trade.

@ Leo, thank you so much for the detailed response as well as the discussion.

Hi again Leo, just looking through all of your really excellent posts and the responses.

My question today is focused on the non-registered account investing, primarily your stock market trading.

I see that you are a really seasoned sophisticated investor using all available methods to increase your net worth and return, which is fantastic

I was wondering if you could please look through all that information for 2016 to post back what the net return % before tax on the non-registered stock trading only (do not include any RE investment). This would be after you’ve paid all the service/carrying charges, interest on the HELOC, margin, loans strictly for non registered stock investing?

Also in the non-registered stock trading account – from 31/12/2015 to 31/12/2016 without the added capital to the account, what was the net increase (pre-tax) after carrying cost/service charges?

Appreciate any response

Thanks

@John, my estimated return for the non-registered account is about 27.71% after interest is deducted based on an average balance of $317,463.33. The Net increase (paper gain after interest expense) is $87,979.78. Hopefully, the table below will make the numbers a bit clearer.

@ Leo, thank you so much for responding as well as breaking down the numbers.

Truly inspiring & I trust others reading & following these post in your blog can learn from your positive drive, enthusiasm and the results that you’ve achieved.

I’m looking forward to seeing the year-end 2017 updates of your non-registered stock market investments.

.

@John, mark your calendar. I think I’ll be looking forward to December 31, 2017.

It looks like you are making great progress. I hope to have progress for my blog by the end of the year.

@Ashlea, the first quarter had been great. Can’t complain. Hopefully, you will make great progress too and share it with us the lessons you’ve learned during the year.